In a Saturday afternoon discussion, I started to think about the macro trends in IT, trying to foresee where AWS & Azure will go. We all know the cloud battles are currently undergoing. We also know that there are very few things we can do to influence them. Still, for some of us, the question is: where we should position ourselves for the future? Perhaps this question is not for the home consumer, but I am sure the IT leaders, the product owners and the business strategists of tomorrow are thinking of it. Hopefully, the directors and managers implementing the strategy are doing it too.

Below you will read a couple of thoughts that did not get into the daily agenda, nor for shaping the strategy for tomorrow. They are personal opinions and do not reflect my past, current or future company views. I would call them recycled trash, even if they are thoughts. Perhaps recycling everything is one of the paths to sustainability, so why not recycle thoughts and ideas too? Of course, as personal ideas usually are, they can be improved! If you want to discuss these topics, feel free to reach out – we will develop better ideas together.

Enough with the introduction. Let’s start with the long term analysis of the cloud battles!

Long term analysis

Technology usually evolves in 4 basic stages:

- Stage 1: Precious

- Stage 2: Personal or Mass adoption

- Stage 3: Utility

- Stage 4: Consumption-waste

I read this idea first in the book Physics of the Future – by Michio Kaku:

Let’s try to think about where Cloud computing currently is. I would argue that we are entering Stage 2: Mass adoption. Would you agree?

The below Gartner chart is the proof of it, the budget that companies will spend on Cloud services will surpass their On-premise budget by 2025.

What stage will follow? Obviously, Stage 3 Utility in which most of the competition will be about price.

From a different perspective, let’s look at the biases of competition based on market demand. Adopting the same method as in “Changes of Biases of competition in disk drive industry” in order to look at the past trends in order to be able to predict the future [The innovator’s dilemma – Clayton Christensen], we have the four main phases of biases of competition for any technology are:

- Functionality

- Reliability

- Convenience

- Price

As per the author, the changes in biases of competition happening in the following sequence: Phase 1: Competition Based on Functionality, Phase 2: Completion Based on Reliability, Phase 3: Competition Based on Convenience, Phase 4: Commodity

In my view, Public Cloud offerings are doing very well in functionality and reliability. Due to their accessibility, scalability, OPEX cost model, feature-rich, easiness of use and improved operational effectiveness, they currently compete on Convenience, as per now. [There are multiple other benefits of Public Clouds, but in order to stay focussed on the topic of the post, I will not detail them here.]

Following the Changes in Biases of the competition framework implies that the next cloud battle will be on price.

I hope you agree that both methods lead to the same conclusion. Even more, the Public Cloud evolving from Stage2: Mass Adoption to Stage 3: Utility is a consequence of the current competition battles on Convenience. The two frameworks are related, though explaining the relationships between them, is not our focus here.

Once the Public cloud becomes a Utility, and perhaps even before that, I would expect the Public cloud providers to strategically position themselves to fuel their need for growth by launching their own products and solutions that duplicate or replace the functionalities of the 3rd party marketplaces provider, entering in the migration services, managed services and consulting services. To some extent, they already are doing that. Look at the following examples:

- Products: Amazon WorkSpaces and Azure Virtual Desktop

- Migration services: AWS Mainframe Modernization and Mainframe and midrange migration from Azure

- Managed services: PaaS, FaaS and Serverless offerings

I observed over time at Azure that they make many partnerships with 3rd party providers to extend the offering of their Marketplace but eventually launch products that directly compete with the partner’s products. AWS is not far from this practice either. We can safely assume that AWS and Azure will do the same for cloud migrations, cloud operations and even cloud consulting, upper and upper on the value chain. They have to once the market for cloud adoption becomes smaller and smaller.

What can we do about the cloud battles?

Business and IT working together!

Well, End to end solutions that bring additional business value to the customers might be a solution for now. They have the same potential as VAS – Value Added Services had Telecom, prolonging the retention of market share until the next disruptive wave.

Nevertheless, either through solutions or not, IT needs to play a bigger role in a company’s strategy. I argue that IT and Business need to work closely together to innovate, adapt, capitalize, operate and preserve sustainable competitive advantages. Perhaps one of the best arguments for Business and IT working together is the following graph summarizing the impact of cloud use cases and improvements on the estimated EBITDA for 2030: https://www.mckinsey.com/business-functions/mckinsey-digital/our-insights/clouds-trillion-dollar-prize-is-up-for-grabs

FinOps and AIOps

FinOps and AIOps might be another solution. They will enable companies to keep their cloud costs in control while increasing profits made from the lean business innovation exercises run in the cloud.

Last but not least: planting the seeds of the next disruption.

Who can be the next disruptor?

Answering this question is a lot harder, as it requires us to look even further into the future. It is a million-dollar question at this point. Unfortunately enough I don’t have enough resources: time and other people’s knowledge to make a complete IT industry analysis.

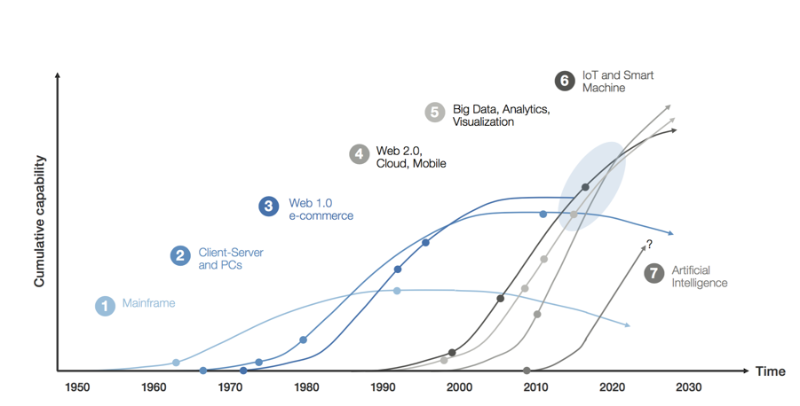

What I can do for now is to look again at the current IT trends:

I would bet that the biggest disruptor will be a company that manages to unify the IoT and AI trends in a framework/product that spreads across industries or a company that harnesses both blockchain and AI. Or even both? The correct answer matters less. What does matter is the common element of almost all the possible scenarios: AI

For the next 20-30 years, my prediction is that: starting from data-driven organizations and incrementally improved AI solutions, all industries will be disrupted by AI.

PS:

Now that I reached this conclusion on my own, I’ll read The Age of AI: And Our Human Future- by Daniel P. Huttenlocher, Eric Schmidt, and Henry Kissinger to confirm, infirm or further improve my conclusions.